Business Overview

In my recent deep dive, I framed Humana as a “great business under pressure”, a company benefiting from a structurally growing Medicare Advantage market but struggling to translate that growth into attractive unit economics.

The Q1 2026 results don’t change that view. If anything, they make the tradeoff more explicit. Humana is still growing, but that growth is no longer the priority.

Bigger, But Not Better (Yet)

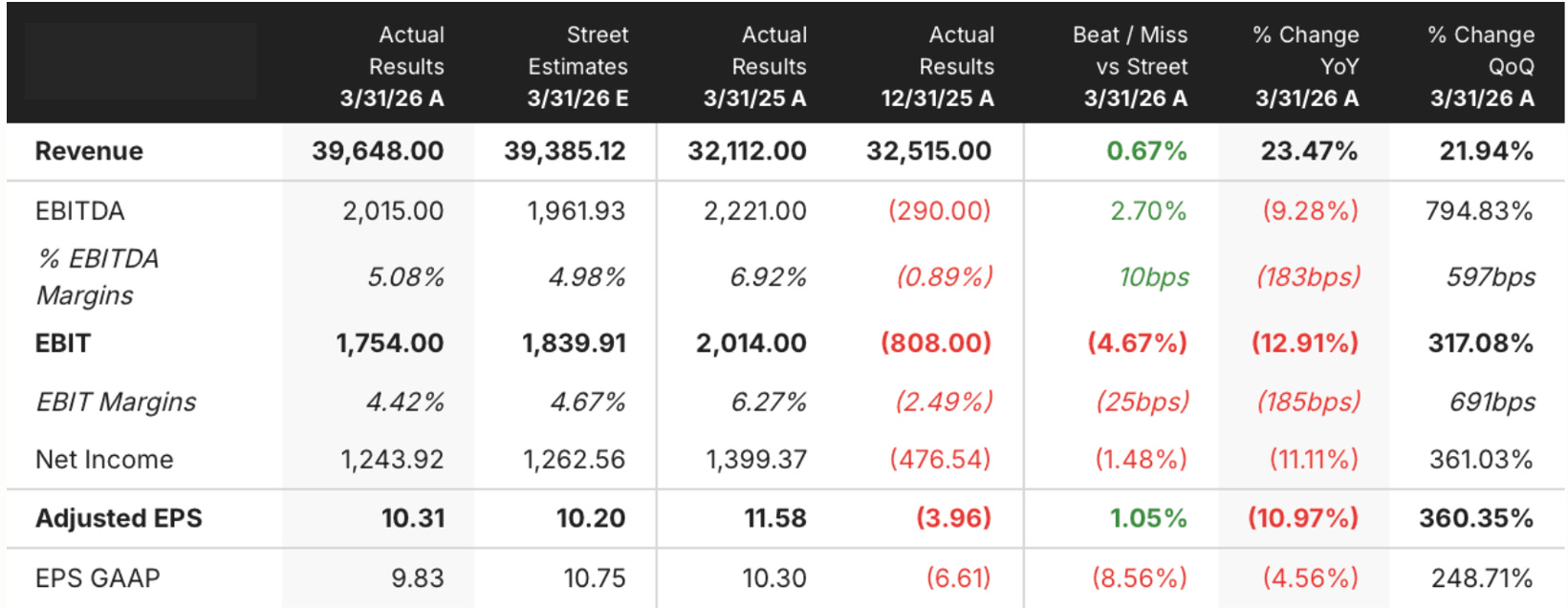

On the surface, the quarter looks strong. Revenue grew 23% year-over-year to $39.65 billion, driven by continued enrollment gains in Medicare Advantage.

But just below the surface, the pressure shows up quickly. Adjusted EPS declined 11% to $10.31. EBIT fell 13% to $1.75 billion. The insurance segment benefit ratio (MLR) came in at 89.4% for the quarter, with full-year guidance holding at an elevated 92.75%.

This is the core tension: the business is scaling, but the economics are tightening.

The Problem Hasn’t Changed

The underlying issue remains straightforward. Medical cost trends are running hot.

Humana is still adding members at an impressive pace, management reaffirmed ~25% individual MA membership growth for 2026. But the incremental economics of that growth are weaker than they’ve been historically.

A Clear Strategic Pivot

The most important moment of the earnings call wasn’t in the financials, it was in how management framed the future.

CEO Jim Rechtin outlined the company’s bidding priorities for 2027 (~16:50 minutes in):

Return to a sustainable margin of at least 3% by 2028

Retention

Growth, a “distant third priority”

For years, the Humana playbook was simple: grow membership, leverage scale, and expand margins over time. Now, the company is effectively reversing that logic. Growth is no longer the engine—it’s the variable being managed.

This is less about pulling back, and more about resetting the foundation.

CenterWell: The Lever That Has to Work

If there is a path back to margin expansion, it likely runs through CenterWell.

The strategy is straightforward: bring more care delivery in-house to better control costs, improve outcomes, and capture a greater share of the value chain.

Q1 showed tangible progress.

CenterWell Senior Primary Care added over 110,000 patients sequentially, driven by both organic growth and the MaxHealth acquisition. The home health segment also expanded its value-based care footprint, now reaching an additional 2 million patients.

This is still early, but it’s directionally consistent with the long-term thesis.

What Matters From Here

Management reaffirmed full-year EPS guidance of at least $9.00, but the next 12–24 months won’t be defined by earnings growth. They’ll be defined by discipline.

Pricing;

Benefit design;

Retention;

And whether CenterWell can help curb Humana’s MLR in a meaningful way.

The Real Question

The investment case for Humana hasn’t disappeared, it’s just shifted. This is no longer a story about how fast the business can grow. It’s about whether the underlying economics can be reset. If they can, the earnings power of the business looks meaningfully higher than what’s reflected today. If they can’t, scale becomes less of an advantage, and more of a burden.

For now, management is focused on the right problem. The question is whether the solution will follow.

NOTE - This is not investment advice. Do your own due diligence.

I make no representation, warranty, or undertaking, express or implied, as to the accuracy, reliability, completeness, or reasonableness of the information presented in this report. Assumptions, opinions, and estimates expressed in this report constitute my judgment as of the date thereof and are subject to change without notice. Projections are based on a number of assumptions, and there is no guarantee that they will be achieved. K9 Investment Research is not acting as your advisor or in any fiduciary capacity.

K9 Investment Research

Healthcare consultant by trade and investor focused on long-term value creation. I write fundamental deep dives on business quality, unit economics, and valuation.